How Do I Start Budgeting?

A budget can help you save money, reduce debt and achieve your other money goals. Start by recording how much you earn each month.

Use bank or credit card statements, paycheck stubs, and benefits statements to determine how much you’re earning and spending. Look back over three months of statements to get the most accurate results.

1. Track Your Spending

To get the most out of your budget, you need to know where your money is going. Fortunately, there are many ways to do this. You can use a spreadsheet, a notebook, an app or even just your bank account statements. Find a system that works for you and stick with it. It may take time to develop a habit of tracking your spending, but it is crucial for taking your budgeting efforts from good intentions to excellent outcomes.

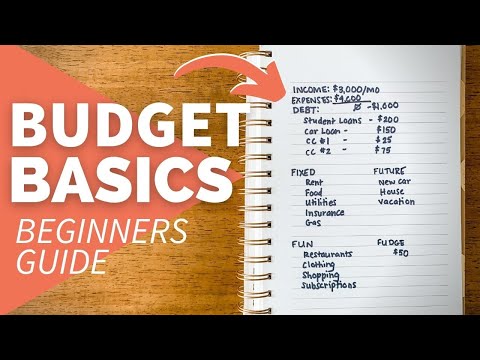

The best place to start is by listing your fixed expenses, items you must pay every month, like a mortgage or rent, utilities, and insurance. You can also list any other monthly obligations you have, like student loan payments or alimony or child support payments. Next, sort your remaining spending into two categories: needs and wants. This step is critical because it will help you prioritize spending and identify opportunities to save or reduce debt. For example, you might decide to drop your gym membership or stop eating out, which would free up funds you could put toward paying off a credit card bill or saving for retirement.

After categorizing your spending, total your income and compare it to your monthly expenses. The goal is to have more income than expenses. If you don’t, it’s time to make some changes.

Whether you are logging your spending in an Excel sheet or with a simple notebook, be sure to record every dollar spent. Then, subtract each expense from your budgeting categories to see how much you have left over. This will help you avoid going over your budget and make it easier to reach your financial goals.

You can also include expenses that happen less frequently than once a month, such as a yearly eye exam or your pet’s vaccinations. You can use your calendar, past credit card statements and other information to determine the average cost of those items each year. Be sure to factor in savings for emergencies, too.

Then, create a budget that lists how much you will save each month and the dates you plan to accomplish each of your goals. If you are working to save for a big purchase or to get out of debt, you’ll want to set a deadline by which you will achieve those goals.

2. Set Goals

When you know how much money is coming in and going out, you can create a budget that helps you reach your financial goals. But creating a budget isn’t just about math—it’s also about record keeping, goal setting, and self-control. That’s why it’s essential to start by creating a goal that’s specific, measurable, attainable and relevant.

To set your budgeting goals, consider what you’d like to achieve in the next month or year. For instance, decide how much you’d like to save each paycheck if you want to save more money,. Then, determine how long it will take you to save that amount. This will give you a clear deadline to work toward and help you stay motivated when it’s time to pull the trigger on those savings.

Then, decide where you’ll put that money. You may want to categorize your expenses to see what categories are eating up most of your income, such as groceries, utilities, and gas. You can also use the information from your credit card and bank statements to help you make this list.

It’s helpful to start with your NET (net) income, which is the money left over after payroll deductions such as taxes and health insurance. This will be the base of your budget and will help you avoid spending more than you earn.

Next, identify your fixed expenses, such as your rent or mortgage, utilities, and car payment. Then, consider your variable expenses, which may vary monthly, such as entertainment and grocery costs. If you’re unsure how to break down your expenses, you can try using a tool to compare similar items.

Finally, create a savings account to address your top priorities. It’s important to make saving a priority so that you can continue to reach your financial goals. If you’re having trouble saving, you may need to adjust your spending habits or find other sources of income. The good news is that once you develop the habit, saving becomes easier and more natural. And if you do go off track, remember that no one is perfect—and making mistakes is okay.

3. Create a Budget

Once you’ve tracked your spending and determined how much money you bring in, it’s time to make a budget. The best way to do this is by listing all your income sources and separating them into fixed and variable expenses. Fixed expenses include rent or mortgage, utility bills, and transportation costs. Variable expenses are those that can change from month to month, such as dining out or entertainment. Once you’ve compiled your list of expenses, be sure to add in any amount you are saving each month, whether that’s into an emergency savings account or to save for a major purchase.

If your projected income is more than your projected expenses, congratulations! That means you’ll have a budget surplus. Depending on your financial situation, you may want to put that extra money into an interest-bearing savings account to ensure it’s there if you need it. Or, you may decide to put it toward a long-term goal or debt repayment. Either way, it’s important to plan for a surplus so you don’t get caught off guard when unexpected expenses arise.

For many people, the easiest way to create a budget is with a spreadsheet program or template. You can find these online or in the app stores. Many feature intuitive formulas that streamline calculations and visual aids to help you see your progress. Some also offer ways to share your spreadsheet with others so you can work together and hold each other accountable.

The next step in creating a budget is to divide your expenses into categories that reflect your needs and wants. For example, you can categorize “utilities” into electricity, gas, and water to help keep track of your monthly bill payments. You can also break down your dining out and shopping expenses into specific line items to identify opportunities for cutting back.

Finally, don’t forget to add in your monthly savings and any other lump sum payments you are making into a budget category. It’s also a good idea to set up an automated transfer from your checking account into your savings account at the beginning of each month to help automate this process and encourage you to stick with your goals.

4. Review Your Budget

Once you’ve nailed down your budget and the financial goals that go along with it, it’s essential to evaluate your budget regularly. Ideally, you should do this at the end of each month, but it’s also good to sit down and assess your overall budget at least once a year. By comparing your budget to your actual expenses, you can determine if you overspent in any categories or have been staying on track with your spending habits.

This step is vital to your success with budgeting but can be frustrating at first. To make this process smoother, it helps to have all of your income and expense data at hand. You can use a spreadsheet, a budgeting app, or even your bank records to get all the necessary information. Once you have the data, it’s easy to spot any differences between your budget and your expenses.

Evaluating your budget isn’t just about identifying the areas in which you need to improve; it’s about determining whether or not the short and long-term savings goals you’ve set are realistic. The best way to do this is to ensure your goals are SMART, which means they’re Specific, Measurable, Attainable, Realistic, and Time-bound.

Once you have your budget and goals in place, it’s time to start saving. A solid savings plan is the most effective way to increase financial stability. By saving a little bit each month, you can build a habit that will help you reach your long-term goals while providing you with peace of mind in the meantime.

Creating a budget may feel overwhelming at first, but it’s a relatively simple process once you know where to begin. To get started, follow the steps outlined above and don’t be afraid to make adjustments as you go along. It takes most people about three months to really get a handle on the budgeting process, so don’t give up and keep trying! The rewards will be worth it in the end. Have you ever tried budgeting? How did it work for you?

Recent Posts

Protecting Your Skin After 60: The Facts About Skin Cancer

Skin cancer poses a serious health threat to elderly individuals, particularly for those aged 60…

The Science Behind Sundowning and How It Affects Seniors

Sundowning is a condition that many seniors face, especially those dealing with memory-related illnesses like…

How Social Casinos Are Changing Gambling

Hey there! Have you ever wondered how social casinos are turning the gambling world on…

Best Games to Play at Wonder Casino

Greetings to all game-playing aficionados! If you're seeking electrifying online casino action, you've gone to…

Typical Uses for Bank Guarantee Characters

Hey there! Let's dive into the world of bank guarantee characters. You might have heard…

Best Online USA Casinos

The best online U.S. casinos offer an expansive selection of casino games and banking options.…